What Is TradingAgents-Astock?

TradingAgents-Astock 是一个基于 TauricResearch/TradingAgents 的 A 股深度特化 fork,由 simonlin1212 维护,面向 Python 开发者、量化研究者和做 A 股研报自动化的人。它把原版偏美股的多 Agent 投研管线改成可直接跑中国市场:7 个 analyst、A 股交易规则、免费直连数据源、pip install 即跑;上游仓库有 65K+ stars as of Feb 2026。TradingAgents-Astock is one of the best AI Trading Agents tools for Python developers, quant researchers, and A-share traders.

Quick Overview

| Attribute | Details |

|---|---|

| Type | AI Trading Agents |

| Best For | Python developers, quant researchers, and A-share traders |

| Language/Stack | Python 3.10+, Streamlit, multi-agent LLM orchestration, HTTP/TCP market-data connectors |

| License | Apache 2.0 |

| GitHub Stars | N/A for the fork; upstream TradingAgents is 65K+ stars as of Feb 2026 |

| Pricing | Open-Source |

| Last Release | N/A — no tagged release exposed in the scraped page |

Who Should Use TradingAgents-Astock?

TradingAgents-Astock is a fit when you need a local, inspectable A 股 research pipeline instead of a black-box SaaS screen.

- Python quant developers building internal research tooling who want a reproducible agent workflow and can wire in their own API keys.

- Indie hackers shipping A-share analysis products who need a ready-made multi-agent backbone without starting from prompt chains or LangGraph wiring.

- CTOs and platform teams that need Chinese-market context, auditability, and a codebase they can extend with custom data sources or strategies.

- Research teams comparing policy, news, and flow-driven signals on Chinese equities where a single-factor backtest is not enough.

Not ideal for:

- Intraday execution systems that need millisecond latency, broker routing, or order management integration.

- Users who need financial advice rather than research outputs; the repo explicitly says it is for learning and technical demos only.

- Teams that want zero LLM spend; TradingAgents-Astock still depends on API-based models for the reasoning pipeline.

Key Features of TradingAgents-Astock

- 7-Agent A-share research pipeline — TradingAgents-Astock expands the original 4-role setup into market, social, news, fundamentals, policy, hot money, and lockup analysts. That matters because A 股 pricing often reacts to regulation, board-level flow, and supply events that do not exist in U.S. equities.

- A-share trading constraints baked in — The trader layer knows about T+1,涨跌停, board lots, ST rules, and market session constraints. That keeps the output closer to what a real A-share desk can actually execute.

- Free direct-market data connectors — The project pulls from

mootdx, Tencent, Eastmoney, Sina, 10jqka, CLS, and Baidu Finance over TCP or HTTP. The page explicitly says there is no Tushare积分墙, no Yahoo Finance dependency, and no external service wall for the market data side. - Dual-LLM architecture —

quick_think_llmhandles the seven analysts, bull/bear researchers, trader, and risk debaters, whiledeep_think_llmis reserved for the research manager and portfolio manager. That split keeps expensive reasoning models focused on synthesis instead of every intermediate step. - Chinese output with English internal debate — The system emits Chinese final reports while keeping the internal debate in English to preserve reasoning quality. That is a practical compromise for teams that need readable output but do not want to lose model performance in multi-agent argumentation.

- CLI plus Streamlit UI — You can run it from

tradingagentsin a terminal or usetradingagents-webin Streamlit. The UI exposes model selection, live pipeline progress, expandable analyst reports, risk review, and PDF export without writing code. - Apache 2.0 and local install — The repo is open-source under Apache 2.0 and supports

pip install -e .for local development. That makes it straightforward to vendor into an internal research stack or patch for custom A-share datasets.

TradingAgents-Astock vs Alternatives

| Tool | Best For | Key Differentiator | Pricing |

|---|---|---|---|

| TradingAgents-Astock | A-share multi-agent research and reporting | Deep A股 specialization with 7 analysts, T+1/涨跌停 logic, and free domestic data connectors | Open-Source |

| OpenSwarm | General multi-agent orchestration | Better fit for generic agent coordination when you do not need market-specific trading logic | Open-Source |

| OpenTrace | Tracing and debugging agent runs | Stronger visibility into agent steps, failures, and runtime behavior than a domain-specific stack | Open-Source |

| Beehive | Collaborative agent workflows | Useful when the goal is multi-agent task coordination rather than a trading decision engine | Open-Source |

Pick TradingAgents-Astock when the output must respect Chinese market structure and you care about policy, fund flow, and unlock risk. Pick OpenSwarm when you want a broader agent runtime that can be adapted to many domains. Pick OpenTrace when your real problem is observability and post-mortem analysis of agent behavior. Pick Beehive when you need a general collaboration layer and not a trading opinion engine.

How TradingAgents-Astock Works

TradingAgents-Astock uses a staged pipeline instead of a single prompt call. The data layer first gathers OHLCV, fundamentals, news, and flow signals from TCP and HTTP endpoints, then seven analyst agents generate domain-specific reports, then bull and bear researchers debate the thesis, and finally the research manager and portfolio manager turn that debate into a position decision.

The design choice is simple: keep low-cost reasoning in quick_think_llm and reserve deep_think_llm for synthesis. That reduces unnecessary token burn while still letting the final decision layer see the full evidence set, which is important when the model needs to reconcile technicals, policy signals, lockup events, and social sentiment.

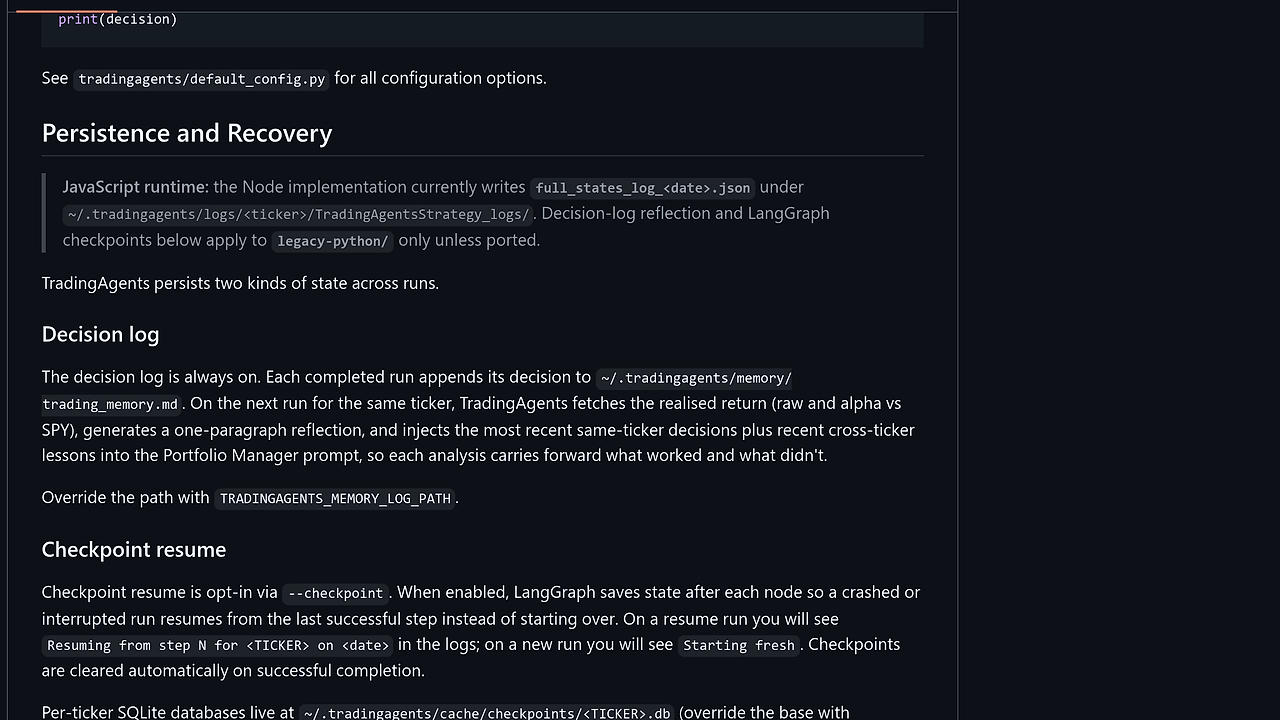

from tradingagents.graph.trading_graph import TradingAgentsGraph

config = {

'llm_provider': 'deepseek',

'deep_think_llm': 'deepseek-chat',

'quick_think_llm': 'deepseek-chat',

'output_language': 'Chinese',

}

ta = TradingAgentsGraph(debug=True, config=config)

final_state, decision = ta.propagate('688017', '2026-05-12')

print(decision)

This example loads the graph, injects a provider config, and runs a full A-share analysis for ticker 688017 on a chosen date. Expect the run to fan out across the seven analysts, then contract back into a portfolio decision object that includes the final Buy/Hold/Sell view and supporting rationale.

Pros and Cons of TradingAgents-Astock

Pros:

- A-share native decision flow — The agent stack understands Chinese market structure instead of pretending U.S. equity rules apply everywhere.

- Large evidence fan-out — Seven analyst roles cover price action, sentiment, news, fundamentals, policy, hot money, and lockups in one run.

- No paid market-data wall — The data layer is built around free domestic sources and direct connectors.

- Inspectability — The codebase is Python-first, so teams can trace prompts, swap models, or add custom tools without reverse engineering a SaaS API.

- Practical UI — The Streamlit front end is usable for analysts who do not want to drive the whole stack from a terminal.

Cons:

- LLM dependency remains — Even though market data is free, the reasoning pipeline still needs paid model APIs for real usage.

- Not a backtester — TradingAgents-Astock is a research and decision layer, not a portfolio simulation engine with execution-grade fill modeling.

- China-market scope is narrow — The specialization is an advantage for A 股, but it is the wrong abstraction if you need U.S. equities or multi-asset coverage.

- Operational cost can rise — The page states each analysis may trigger 30–50 LLM calls, so heavy usage needs budget control.

Getting Started with TradingAgents-Astock

The fastest path is a local editable install followed by a CLI or Streamlit run. You only need Python 3.10+, the repo checkout, and an API key for the model provider you plan to use.

git clone https://github.com/simonlin1212/TradingAgents-astock.git

cd TradingAgents-astock

pip install -e .

# optional model extras

# pip install -e .[google]

tradingagents --help

tradingagents-web

After install, create a .env file with your LLM provider key and choose a provider in the config or UI. The first run will fetch market data from the free connectors, execute the analyst chain, and render the report in either the terminal or the browser at http://localhost:8501.

Verdict

TradingAgents-Astock is the strongest option for A 股 research automation when you need the original TradingAgents multi-agent design plus China-specific market rules. Its best strength is the 7-agent pipeline with free direct data sources; its main caveat is the continued dependence on paid LLM APIs. Recommended if you want an inspectable A-share analysis stack you can run locally and extend.